Everything’s a Shitcoin: The Citrini Condition

Harder, better, faster, stronger

On Feb 22, 2026, Citrini Research published ”a scenario, not a prediction,” and broke the internet.

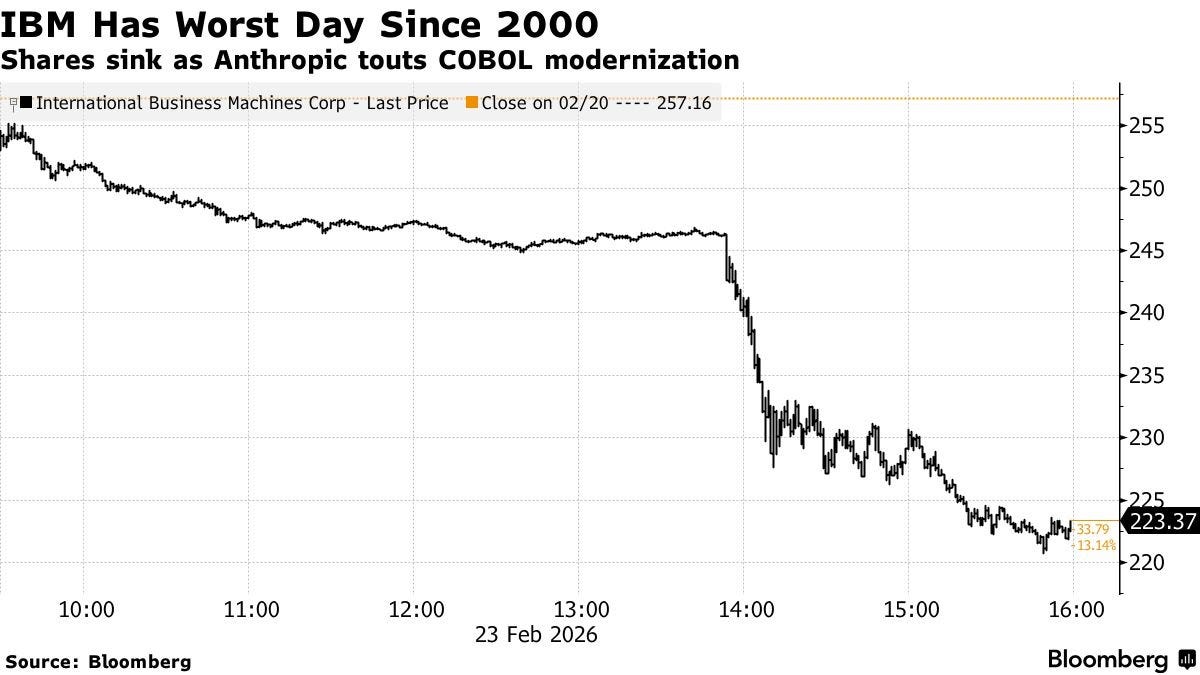

The Dow lost 822 points that day (1.7%), software stocks dropped 9% or more, IBM had its worst single-day performance since 2000, DataDog, CrowdStrike, and Zscaler cratered, and The Wall Street Journal – the WSJ (!) – ran a front-page story: “Viral Doomsday Report Lays Bare Wall Street’s Deep Anxiety About AI Future.”

The “scenario” was exactly what they claimed it wasn’t: bear porn [and] AI doomer fan-fiction. Sure, it extrapolated further and with a better grasp of financial markets than AI2027. Its authors clearly understand the arcane details of underwriting private credit and how that might impact who ultimately holds the bag if it all goes bust (answer: nobody knows). They moved through the different layers of social, economic, and financial implications like an AI-focused chapter in “Devil Take the Hindmost,” or “When Genius Failed” but about the apocalyptic consequences of AI.

Those are great books worth reading, and, if I’m being honest, so is Citrini’s article! Seriously, read it! So what’s the problem, then? Why are we all devoting so much time to this article and its implications?

Well, a single Substack post had a meaningful impact on the deepest and most liquid global markets within 24 hours.

Which means the problem is this: everything’s a shitcoin now.

Everything’s a Shitcoin Now

This kind of breathless, nervous, “sell-it-all-with-haste” volatility has long been reserved for another asset class: crypto.

Lacking any serious “fundamentals,” crypto tokens trade (traded? is crypto over now?) on “narrative” and “vibes.” Massive swings in price are common (to both the up- and down-side), and speculative traders hoping to hit it big for the rare “1000x” that will “retire your bloodline” and help one “escape the permanent underclass” continue bidding on what became known over time as “shitcoins.”

But everything’s a shitcoin now.

As we’ve written before, the money being poured into AI can’t be “justified” like a typical investment. The future cashflows required for the megalabs to return anything on invested capital are almost literally inconceivable. Instead, it’s humanity yet again deigning to play God, and “flirting with the creation of something powerful enough to transcend us.”

In other words: much of the AI industry is trading on “narrative” and “vibes.”

[Just to be clear: we believe in the power of AI – we’re an AI fund – but that doesn’t mean certain companies in the industry don’t have inflated valuations]

What’s crazy is the market knows it’s all a ruse. Talk of a bubble and collapse and catastrophe is natural. It’s like the entire world is in the conference room scene at the beginning of Margin Call, waiting for the music to stop.

Which is why everything’s trading like a shitcoin. Speed is the name of the game (and has been forever). But now we have ultra-competent machines trading news almost instantly, too. Couple that with increasingly-open access to financial markets, the roaring popularity of ODTE options, sports betting, and prediction markets and we have ourselves a fully operational casino performing at the speed of light!

Anthropic & The Long Shadow of Claude

Take Anthropic, for example. On Monday, IBM crashed because Anthropic announced “Claude Code could be used to automate the exploration and analysis work that drives most of the complexity in COBOL modernization, a key IBM business.”

A publicly-traded company worth ~$250B lost 13% in a matter of hours. $~30B of market cap eviscerated.

And there’s more!

Plug-ins for Claude Cowork caused a market selloff

Announcing Opus 4.6 caused a selloff

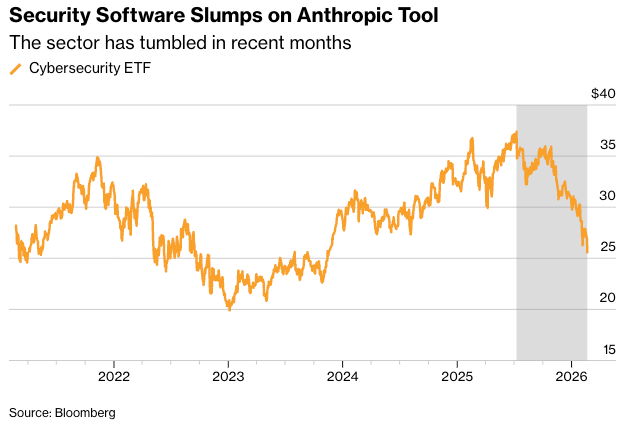

Claude Code Security caused cybersecurity stocks to decline

CrowdStrike fell 11%. Cloudflare dropped 9.6%. ID company SailPoint slid ~8%

In a trend that would make “Mr. Misanthropic” proud, whereas excitement about OpenAI and ChatGPT led the market up, excitement about Anthropic and Claude seem to be driving the market down. Across these episodes, markets erased roughly $800 billion on AI narrative alone.

But of course, stocks aren’t just going down! There have been many instances of stocks going up in value because of AI narrative, too. The most prominent example was Oracle, which gained 36% in a single day back in September of 2025, adding $244B in value to its market cap. It has, however, given everything back (and more) since then, because of course it has! Everything’s a shitcoin now.

Infrastructure for Shitcoins

There have always been short sellers. In fact, some believe that shorts are critical for healthy markets to function, promoting liquidity, stabilizing markets, permitting risk management, and acting as the natural “watchdog” for nefarious activity in a laissez-faire system.

Shorts like Citron, Hindenburg (now disbanded), Kerrisdale, and others are activists, taking positions against companies they feel are overvalued and publishing research that supports their opinion in the hopes that the reaction makes them money. Everything here is legal, and as I mentioned, often healthy.

These shorts, however, typically expose actual fraud or provide evidence for the over-valuation of a given security. But when everything’s a shitcoin, properly-positioned investors can even benefit from “a scenario, not a prediction.”

In the credits for the Citrini piece, the authors thank Sam Koppelman for help with proofreading. Koppelman co-founded Hunterbrook Media, an investigative newsroom attached to Hunterbrook Capital, a hedge fund. A newer take on activist short selling, the newsroom produces independent, investigative content that the fund is free to take positions on before publication. The reporting need not always be published with the specific goal of informing the fund’s positions – it’s a newsroom focused on open-source investigative reporting based on publicly-available information. Again, entirely legal and perhaps even healthy! We don’t even know if Hunterbrook was positioned ahead of the article or not. But the coincidence is fascinating.

The real distinction here is between fact and fiction. Activist short sellers typically hope to profit from exposing facts that demonstrate illegality, fraud, or wrongdoing. If - and only if – Hunterbrook was positioned for a reaction to this article, it may be the first time a fund has profited from publishing a hypothetical situation that anticipates a fictional future.

The “Other” Narrative: Academics & Human Ingenuity

Alex Imas at Chicago Booth examined more seriously the conditions under which AI could produce negative growth. That piece is also worth a read, but it’s long and technical, so it doesn’t move markets as much.

He proposes two mechanisms for negative growth:

Demand collapse via redistribution

Immiserating growth via capital decumulation (from Benzell et al.’s “Robots Are Us“)

Both models identify real economic forces, but the conditions for actual negative growth are extreme – near-total automation, no policy response, no new categories of demand, no institutional adaptation. More realistically, these forces will drag AI-driven growth toward the lower end of forecasts rather than reverse it entirely.

He ultimately concludes that though the mechanisms are real, the conditions required for actual sustained negative growth are too extreme to hold in practice. To start, no productivity-led recession has ever occurred, which is the classic rebuttal: no, this time actually isn’t different. Spreadsheets expanded the number of analysts, ATMs expanded bank branches, cloud computing expanded the startup ecosystem, etc. Historically, productivity tools create more economic activity, not less.

The key variable is diffusion speed versus adjustment capacity. AI may be different because it diffuses faster than previous technologies. Nobody knows the answer yet, which means the set of possibilities is enormous, which is, again, why everything is trading like a shitcoin.

The Kobeissi Letter published a counter-piece arguing the bull case for AI. As David Friedberg has often mentioned in the All-In pod, Kobeissi writes that “it is important to remember that humanity has ALWAYS prevailed; and the free market ALWAYS works itself out.” History suggests it’ll all be ok! The same AI disruption being priced as collapse is actually the start of the largest productivity expansion in history. The market is underpricing abundance.

In perhaps the most spiritually aware response to this situation, Will Manidis published a critique calling the Citrini piece “Randian genre fiction” that treats markets as impersonal forces when they are actually choices made by people with names. He argues that both the panic and the optimism wrongly treat AI as a force of nature – a storm that arrives impersonally against which we’re powerless to choose.

He notes that blindly subscribing to that worldview, powerlessness in the face of change, is the most dangerous dynamic of this situation. To his credit, this line of thinking informs Peter Thiel’s position that the illusion of powerlessness makes room for demagogues that he likens to the arrival of “the Anti-Christ.”

Harder, Better, Faster, Stronger

“Harder, better, faster, stronger” came out in 2001. Daft Punk found some real product-market-fit in the new century. Since 2001, we’ve gotten the dot-com crash, the cloud and mobile computing paradigms, social media, the GFC, crypto, COVID, and now AI. In just over two decades.

Markets are converging, nobody knows where to put their money, and as a consequence, everything’s a shitcoin.

Harder, better, faster, stronger, indeed.