AI Waves #10: The frontier goes public, the labs ship the agent, and inference gets repriced

Capability is still ahead of capital.

May 22, 2026 | Nazaré Ventures

Previous issues: #1 | #2 | #3 | #4 | #5 | #6 | #7 | #8 | #9

The frontier goes public

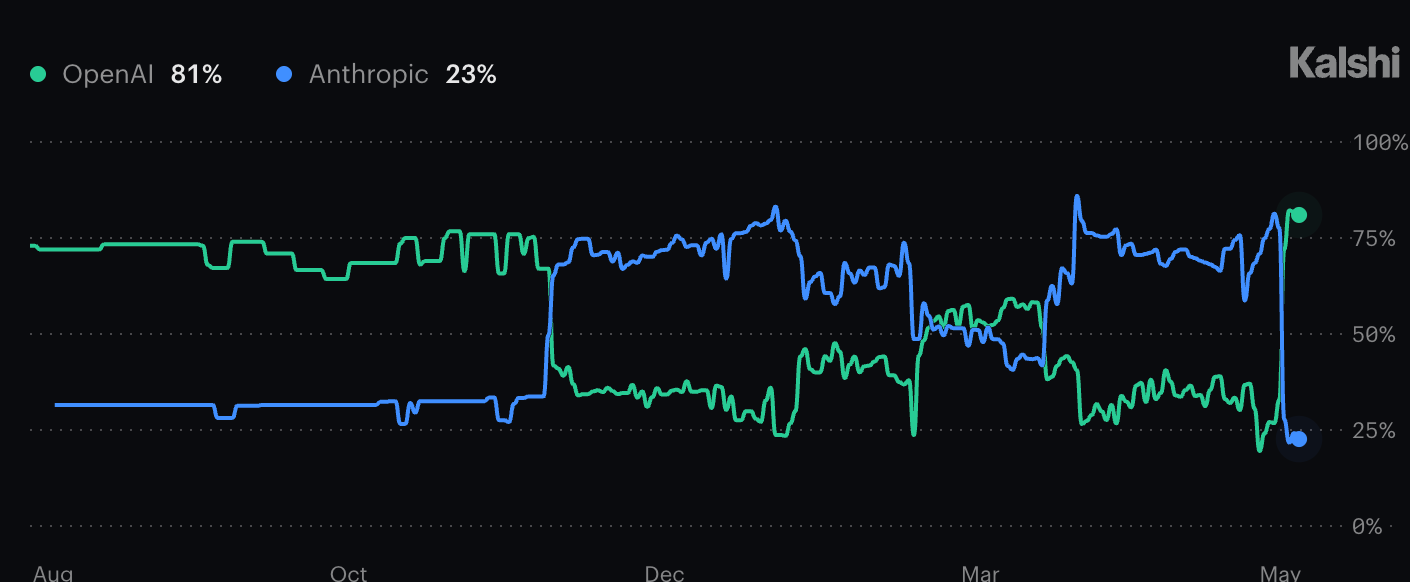

For a decade, the trend has been stay private for longer. Stripe, Databricks, and others absorbed hundreds of billions in private capital and avoided the disclosure burden, the quarterly pressure, and the shareholder noise that come with a public listing. The frontier labs are about to break that trend. SpaceX’s S-1 became public May 20, with a $28.5 trillion claimed total addressable market and a mission statement that includes building the systems “to extend the light of consciousness to the stars.” OpenAI is preparing a confidential filing within weeks, possibly Friday, with Goldman Sachs and Morgan Stanley working toward a September listing at a valuation potentially exceeding $1 trillion. Kalshi gives OpenAI 83% odds of beating Anthropic to public markets. Anthropic is in talks to raise at least $30B at $900B, with the round expected to close by month-end, and is targeting an October listing. The three largest private AI franchises are all moving to public markets in the same quarter.

The reason is capital scale. OpenAI initially touted $1.4 trillion in infrastructure commitments in late 2025, since walked back to roughly $600 billion by 2030, still the largest physical-buildout commitment any AI lab has put on paper. The Anthropic-SpaceX Colossus lease, disclosed for the first time in the S-1, runs at $1.25 billion per month through May 2029, roughly $40 billion total. The hyperscalers around them are guiding capex at hundreds of billions annually. The S-1 also disclosed that SpaceX holds an option to acquire Cursor for $60 billion in Class A stock. Private markets are deep but not infinite at these magnitudes. The “staying private for longer” thesis applied to firms whose growth could be funded inside the private system. Frontier AI is not one of those firms.

The labs are shipping the agent

Last week covered the consulting partnerships: Anthropic’s $1.5B joint venture with Blackstone, OpenAI’s DeployCo built around Tomoro’s 150 forward-deployed engineers. The move confirmed the argument I made in Models Aren’t Moats: the labs themselves understand that models alone are not the moat. This week they went further. Anthropic launched Claude for Small Business on May 13, a packaged agent running inside Claude Cowork that handles payroll planning, monthly close, invoice chasing, lead triage, and contract routing across QuickBooks, PayPal, HubSpot, Canva, DocuSign, Google Workspace, Microsoft 365, and Slack. OpenAI placed Codex and ChatGPT under Greg Brockman’s unified product leadership and added a personal-finance agent inside ChatGPT Pro through a Plaid integration covering more than 12,000 financial institutions. Google announced Gemini Spark at I/O, an always-on agent across Gmail, Docs, Workspace, and Chrome, alongside the Universal Cart that runs on top of Google’s Universal Commerce Protocol, an open standard for agentic commerce now governed by a tech council that includes Amazon, Meta, Microsoft, Salesforce, Stripe, Shopify, Etsy, Target, and Wayfair as of April.

Forward-deployed engineers install and tune the agent inside a customer’s stack. The agent is what they install. The labs now hold the model, the agent product, the deployment apparatus, and the default distribution surface.

The protocol layer is the new piece. UCP, governed by every major hyperscaler and marketplace, sets a shared standard for agent-merchant interaction underneath the individual harnesses.

It is incredibly early. The labs have not won the application layer. They have entered three new sections of it. The question for application-layer companies after this week is which spaces the labs are coming for, and which they aren’t.

Inference is being repriced

Agents drive the repricing. They are expensive to run, and the labs are now running them at scale. Inference as the binding constraint is a year-old consensus. JP Morgan sizes the inference market at 10 to 50 times training. The receipts arrived this week.

Anthropic reported Q1 revenue of $4.8B with a projected Q2 of $10.9B and a projected operating profit of $559M, reaching breakeven roughly two years ahead of internal plan. Dario Amodei said the company had planned for 10x annual expansion and hit 80x in Q1, growth he described as “too hard to handle.” The company also announced a $200/month Agent SDK credit starting June 15, framed as free but community-noted as an effective price hike for power users running programmatic workloads through subscription-tier accounts. Google disclosed at I/O that monthly tokens processed across its products went from 9.7 trillion in May 2024 to 480 trillion in May 2025 to 3.2 quadrillion in May 2026. Pichai’s note: “never imagined I’d say quadrillion in an I/O keynote, but here we are.” SpaceX’s S-1 priced the Anthropic-Colossus arrangement at $1.25B per month through May 2029. OpenAI launched Guaranteed Capacity, letting enterprise customers reserve long-term access to OpenAI compute on one-to-three-year commitments with tiered discounts. Cerebras priced at $185, above its already-raised $150-160 range and well above the original $115-125 band, 20 times oversubscribed, and closed its first session at $311 (+68%), at a ~$48.8B implied valuation.

What started as scattered receipts last year is consolidating into a shape. Anthropic’s Q2 profitability shows the unit economics of running frontier-scale capacity for its own products. Google’s quadrillion-token disclosure maps the consumption surface across an entire hyperscaler’s product line. The $40 billion Colossus lease is the largest single bilateral compute arrangement on record and is now priced through 2029. Guaranteed Capacity turns long-dated compute into a recognized SKU with tiered enterprise discounts. Cerebras priced hardware the public market bid up 68% on day one. Long-dated compute is becoming a tradeable line item, and the labs are the ones setting the price.

Inference is one of several things agents need to work. Memory, verification, and coordination are the others. None have collapsed into a single dollar figure the capital cycle can price the same way. The current cycle prices the dimension with a clear unit of consumption: tokens. At I/O, Demis Hassabis identified data as DeepMind’s binding constraint, and Google has begun selling TPU capacity externally as a consequence.

The receipts this week tell us inference is being priced. They do not tell us inference is the only thing that ought to be priced.

The pushback has crossed into policy

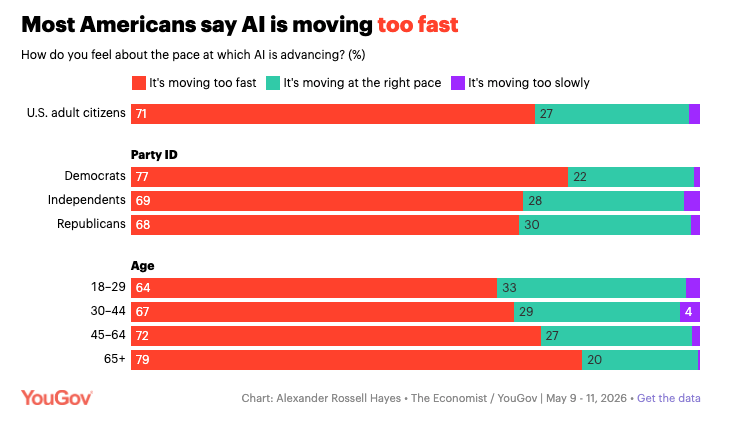

An Economist/YouGov survey this month found 71% of Americans believe AI is moving too fast (68% Republicans, 77% Democrats). The Harris Poll 100 shows OpenAI’s partisan-favorability gap widening from +1 in 2024 to +12 in 2026, with Anthropic the lone structural outlier. Morgan Stanley described public pushback this week as “a binding constraint, particularly around data center buildout” in its midterms note. Public sentiment is now a line in capex models.

The White House followed. The Office of the National Cyber Director briefed Anthropic, OpenAI, and Reflection AI on a forthcoming executive order; under the voluntary framework, frontier labs would share advanced models with government agencies up to 90 days before public release. Trump postponed the signing on Thursday, saying he “didn’t like certain aspects” and that the order “gets in the way.” Even the soft version of the framework was too much for the administration to sign this week. The framework remains on the table.

Meta laid off 8,000 employees this week and reassigned 7,000 more to AI teams. More than 1,000 surviving staff signed an internal petition opposing the Model Capability Initiative and the Agent Transformation Accelerator, the mouse and keystroke tracking software Meta installed on company machines to train AI on human computer behavior. The petition cited the National Labor Relations Act. Standard Chartered CEO Bill Winters described 8,000 AI-driven role eliminations as “replacing in some cases lower-value human capital with the financial capital and investment capital we’re putting in.” Former Singaporean President Halimah Yacob called the framing “disturbing” and “demeaning” on Facebook within 24 hours. Regulators in Hong Kong and Singapore both asked Standard Chartered to clarify. Winters walked the comments back. Eric Schmidt got booed at his University of Arizona commencement on May 16 when he told graduates “when someone offers you a seat on the rocketship, you do not ask which seat, you just get on.” Booed again when he tried to recover with “if you’d let me make this point, please.”

The polling and the framing line up. People being told to accept replacement are the same people telling pollsters AI is moving too fast. The buildout still needs them to buy in.

Math is the leading indicator

This week, an internal OpenAI reasoning model disproved Paul Erdős’s 1946 planar unit distance conjecture, constructing a family of configurations using Golod-Shafarevich theory and infinite class field towers that improve polynomially over the long-presumed square-grid optimum. Princeton’s Will Sawin pinned the improvement to n^(1+δ) with δ ≈ 0.014. The argument runs 125 pages, with a 19-page companion paper signed by nine leading mathematicians: Noga Alon, Thomas Bloom, Tim Gowers, Daniel Litt, Sawin, Arul Shankar, Jacob Tsimerman, Victor Wang, and Melanie Matchett Wood. Gowers, the Fields medalist, called it “a milestone in AI mathematics.”

The signal worth noting: Thomas Bloom called OpenAI’s October 2025 math claim “a dramatic misrepresentation.” He now signs the paper. His line on the new result: “AI is helping us to more fully explore the cathedral of mathematics we have built over the centuries.”

OpenAI’s Alex Wei: math is a leading indicator of what is to come. A general-purpose model just autonomously disproved an 80-year-old argument. That is the early look of “Level 4” AI: systems making original contributions across fields, not just speeding up existing work. Capital, politics, and the application layer are repricing what is already in the world. Capability keeps producing what is not.

What We’re Watching

Pope Leo XIV’s Magnifica Humanitas drops Monday May 25.** First encyclical on AI and human dignity. Signed May 15, the 135th anniversary of Leo XIII’s Rerum Novarum (1891). Presented at 11:30am at the Vatican Synod Hall, with Cardinal Víctor Manuel Fernández (Doctrine of the Faith) and Cardinal Michael Czerny (Integral Human Development) as main presenters, and Anthropic interpretability lead Chris Olah on the speaker panel alongside theologians Anna Rowlands (Durham) and Leocadie Lushombo (Jesuit School of Theology / Santa Clara). Cardinal Pietro Parolin (Vatican secretary of state) concludes.

Anthropic acquired Stainless for $300M+ on May 18.** Developer-tooling platform whose customers included OpenAI, Google, and Cloudflare, now being wound down and absorbed into Anthropic’s stack.

Sam Altman offering YC founders $2M in OpenAI tokens for equity.** All 169 startups in YC’s Spring 2026 batch, uncapped SAFE, 1-4% equity expected at Series A. Altman called it “tokenmaxxing.” Pre-IPO cap-table consolidation across the lab cohort.

Portfolio

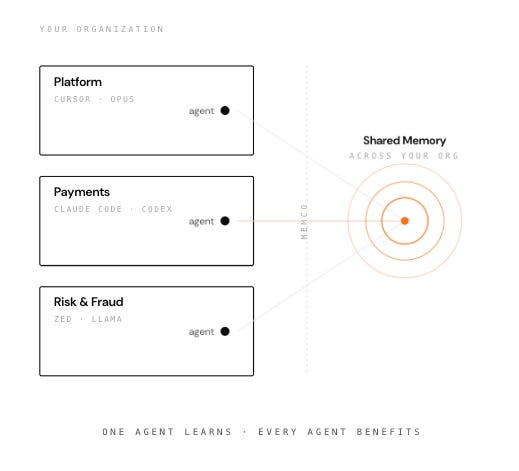

New portfolio company: Memco. Nazaré joined Memco’s pre-seed round. Memco is building the shared memory layer for AI agents. Every agent stack shipped to date has been missing this primitive. Agents that get smarter at runtime still start every session from zero. Cursor doesn’t talk to your CI pipeline. Your teammate’s webhook fix dies in a closed PR. The next agent rediscovers the bug your last agent fixed last week. The category sharpened this week alongside the rest of the stack. Agents that don’t share memory pay full token cost on every interaction, and that cost is what is being repriced.

Memco’s first product, Spark, captures real developer experience (intent, failed attempts, eventual fix) and makes it reusable across IDEs, CLIs, and CI pipelines, with public and private memory layers that let teams choose between rented context and owned context. Published benchmarks (arXiv 2511.08301, 200+ evaluation runs across SWE-Bench variants and DS-1000) show 40% token reduction, 34% faster execution, and 30B-parameter models matching frontier-class systems when augmented with shared memory. The team is led by CTO Valentin Tablan with Scott Taylor and Kristoffer Bernhem. Incubated by Moonsong Labs.

Prime Intellect: the research loop is automating. Three pieces in seven days. On May 14, Autonomous AI research for nanogpt speedrun, where an agent ran the full ML research loop and improved the open-source nanogpt speedrun benchmark by stitching together community PRs. On May 18, General Agent: A Self-Evolving, Synthetic Agent Environment, an environment that generates and refines its own training data. On May 20, Systematic Reward Hacking and Prime Sprints, a crowdsourced research platform built on Lab. Anyone proposes an experiment, agents manage the queue, top projects win $5K+ in compute credits. First track: a detailed paper on the physics of reward hacking showing predictable scaling patterns and granular-scoring mitigation. Experiments run for under $1 and under 30 minutes on small models. Capability research is itself becoming automated, and Prime Intellect is shipping the infrastructure for it.

Vast.ai: the SDK for agents that buy their own compute. Vast.ai shipped a Python SDK this week, marketed directly at AI agents that provision their own GPU compute with no human in the loop. Three lines of Python to search offers, launch instances, and manage running workloads. Three pricing signals from the same exchange underneath: H100 hourly up 18% week-over-week to a median of $2.51 (tight supply), Flux.1 diffusion workloads on RTX 4090s at ~$0.40 per hour with 48 cards available, and Unsloth Studio integration delivering 2x faster training at 70% less VRAM.

Dimensional: a 48-hour robotics build in Shanghai. Dimensional and muShanghai co-host a robotics hackathon May 26-28, with 10+ Unitree robot dogs deployed across swarm routing, autonomy, navigation, and agent integration. Winner takes home a Unitree Go2. Event page, announcement.

@ muShanghai: Robot Hackathon")

LayerLens: the capability surface is jagged. LayerLens published findings on May 20 showing how unevenly model capability lands at the task level. Gemini 3.5 Flash scores 96%+ on AIME and MATH and 0% on SWE-bench Lite. Mistral Medium and Large differ by 53 points on HumanEval. The headline aggregate numbers hide that models are highly specialized, and a single capability score buys nothing in production. The eval-as-infrastructure pitch from last week’s SubQuadratic partnership is the same pitch with new receipts.

Intelligent Internet: opencode-a2a ships. II released opencode-a2a on May 15, exposing OpenCode through the Agent-to-Agent protocol with an inbound server surface and embedded outbound client. Drops alongside psql_bm25s from last week as part of the II open-source agent-coordination stack.

Closing

Last week, compute itself became a tradeable contract on the CME. This week the labs that consume that compute filed to go public. The capital cycle is repricing the infrastructure faster than the infrastructure ships. The most credible technical statement of the week was not from the IPO desk. It was a 125-page proof. Capital, politics, and the application layer are repricing what is already in the world. Capability keeps producing what is not. Capability is still ahead of capital.